Selling life insurance is already cumbersome, so why even bother adding to it?

I’m a life guy, have been for 40 years selling over $1B of face amount. From the very beginning I concentrated on building my business by finding unique niches that made my value proposition more attractive to prospects. Once I earned their trust and confidence their generous referrals lead to alignments and introductions to complimentary, non-competing professionals. These two things reduced or eliminated competition wherever possible while allowing me to earn a respectable living for my efforts.

The life insurance sale process presents numerous challenges regardless if the insured is a cold prospect or an established client. Why? You need to prove the need is there, that your solution is the best one and you’re the one to fill it while “separating them” from their money. As a result, most agents avoid making the additional pitch for life insurance in order to avoid complicating a sale. While I continue to write life insurance regularly, Life Settlements have eliminated every obstacle I’ve encountered in my four decades of industry involvement.

So why bother? On average 6 out of 7 life insurance policies are terminated. Advisors miss out on opportunities to help qualified clients sell this valuable asset while avoiding potential E&O issues. This scenario happens more often than you might think.

Sometimes the path of least resistance is not the most lucrative one. Let’s look at this nearly missed opportunity. An insured decided to terminate her life insurance policy which had outlived its intended purpose and was under the assumption, according to the carrier, surrender was her only option. Value had she done so? $0. Neither she nor her family and advisors ever heard of life settlements.

Negotiated result?

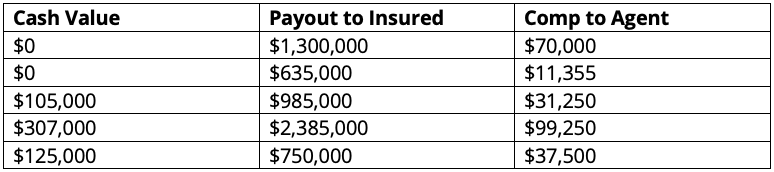

- $800,000 from the sale PLUS $197,000 refund of the premium she recently paid.

- A total of $997,000 for a contract thought to be worthless.

And the referring ASNOA Rep?

- He invested no time beyond opening the discussion and referring the case to me.

- Gross compensation paid to us? $37,500

Additional examples of successful results:

Remember the last policy you sold, the hours involved, and the expenses incurred? Were you rewarded with comp at these levels?

Independent Agents Have A Leg Up on Selling Life Options

Your clients already trust you with their assets. The typical independent insurance agent retains 80-90% of clients because of the selection of products, coverages, and price a non-captive agent can provide. According to a LIMRA study, multiline agents have a client base at least double that of all other types of financial professionals. The average book consists of a loyal, trusting client base both higher in number and more diverse in age. In other words, the perfect environment for life settlements. The challenge most agents encounter, a foundation of trust and confidence, isn’t an issue. Now all you have to do is bring up the subject of life settlement.

What Can You Do Today?

I can assure you cases are sitting in your book. Each one of you has a significant number of prospects both hidden and out in the open – policies you sold as well as those you didn’t. Think about your clientele, your circles of influence, client’s CPA/JD, social networks, essentially everyone you come into contact with.

Just mention it. Just ask. Once you find them – and you will – give us a call and we will run with it on your behalf.

Marc Ruskin, ChFC, CLU, REBC, RHU

Director Life Settlements

Contact Marc

Learn more about Marc Ruskin and Life Settlements by clicking here.